Top Down #1: Capex Upcycle

19th June 2025

The Top-Down Series is a new initiative we have undertaken to make investors understand how they can distill the macro picture into action.

Investing with a top-down approach means starting at the macroeconomic level—identifying the big-picture trends—and then drilling down into the most promising sectors and stocks.

#1 Capex Upcycle

What Is a Capex Cycle?

A capex cycle refers to the ebb and flow of corporate and government spending on fixed assets—factories, power plants, roads, data centers, etc. It typically follows four stages:

Why India’s Capex Upcycle Matters Now?

Policy thrust: Governments are accelerating infrastructure monetisation and green-energy targets, unlocking private capital.

Corporate balance sheets: Strong cash flows in power, telecom and manufacturing mean Indian companies can self-fund much of their expansion.

Global supply chains: Multinationals are diversifying out of China, boosting India’s manufacturing and logistics capex.

According to Crisil, India will channel nearly ₹17.5 lakh crore into renewables, roads and realty over FY26–27. S&P projects corporate capex to double to $850 billion by 2030. This coordinated wave of spending signals the Expansion phase of the capex cycle—an ideal backdrop for top-down investment.

Five Sectors for India’s Next Capex Wave

Source: Fortune India

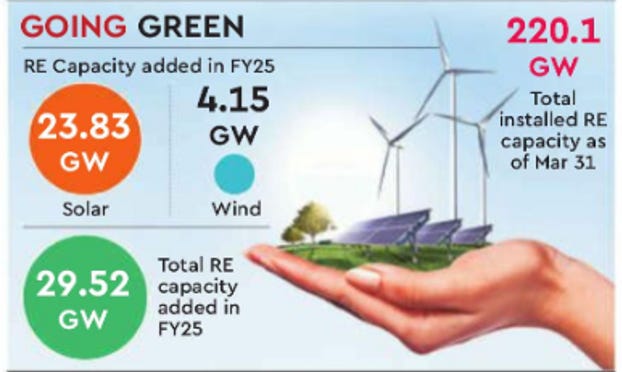

1. Renewable Power Generation

Dominant share: Power generation alone is projected to absorb nearly 28 percent of all corporate capex through 2030, with renewables forming the lion’s share of that bucket.

Massive capacity additions: In FY26 and FY27, India plans to add about 75 GW of green energy capacity—with storage-linked “hybrid” projects accounting for roughly 37 percent of the new buildout—fueling both carbon targets and reliable 24×7 supply.

Monetization & private participation: As utilities and project owners unlock value via asset-monetization routes, fresh equity and debt will flow into clean-energy players, making this the single biggest capex theme.

Source: Financial Express

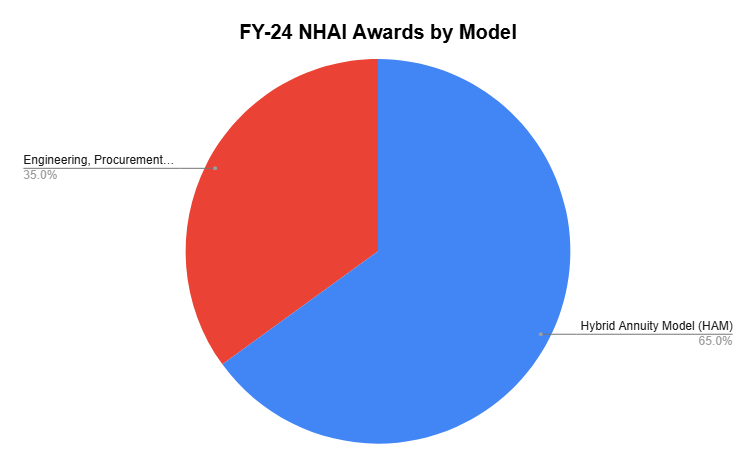

2. Road & Highway Infrastructure

Pre-pandemic highs: The National Highways Authority of India (NHAI) is on track to award around 6,000 km of new projects per year—levels last seen before COVID.

Growing hybrid funding: Proceeds from toll-road monetisation are set to account for nearly 18 percent of NHAI’s funds in the next two years (up from 14 percent earlier), drawing institutional capital into proven cash-flow assets.

Long runway: With traffic volumes still below potential and ambitious corridor expansions in the pipeline, roadbuilders and EPC contractors stand to benefit for years to come.

3. Transmission & Grid Expansion

Critical enabler: As renewables surge, timely grid upgrades are essential. Transmission capex is expected to make up roughly 10 percent of India Inc.’s total investment over the next half-decade.

System resilience: Strengthening inter-regional links, adding high-voltage direct-current corridors and building hybrid charging points all play into a sustained capex cycle for utilities and equipment suppliers.

Policy tailwinds: Regulatory push for open-access networks and faster tariff approvals will help clear project bottlenecks and accelerate spend.

4. Real Estate & Construction Materials

Revenue growth: Developers’ top-line is forecast to climb at 10–12 percent annually in FY26–27, underpinned by robust housing demand and healthier land-monetization strategies.

Debt discipline: Strong operating cash flows in residential and commercial segments have kept leverage under control, paving the way for fresh launches.

Cement’s role: While cement accounts for around 5 percent of total capex in the broader corporate universe, its pivotal role in both infrastructure and housing makes it a proxy for construction-cycle strength.

5. Core Energy & Mobility (Oil & Gas | Airlines)

Oil & Gas: Upstream, refining and pipeline expansions are slated to absorb about 10 percent of capex through 2030, as India secures energy self-reliance and adds petrochemical capacity.

Aviation: Carriers led by IndiGo and Air India plan to invest an estimated $75–100 billion in new aircraft over the next decade—triple their current fleet size—to meet surging passenger demand.

Leverage mitigation: Much of this spend will be lease-financed, helping airlines manage balance-sheet impact while modernizing fleets.

Source: Upstox

With policymakers and corporates channeling record funds into power, roads, grids, property and core energy & mobility, these five sectors offer both scale and policy support. For investors seeking exposure to India’s capex upcycle, focusing on high-quality names within these themes can capture the growth and structural tailwinds driving the economy forward.

Disclaimer

All information is sourced from publicly available data, and while every effort has been made to ensure the accuracy and reliability of the information provided in these notes from the management meeting, Ayush Agarwal Research cannot guarantee that the information is complete or free from errors.

I, Ayush Agrawal, am registered with SEBI as an Individual Research Analyst under the registration number INH000013013, effective from September 14, 2023.

I offer paid research services to my clients based on this certification. Opinions expressed otherwise regarding specific securities are not investment advice and shall not be treated as recommendations. Neither I nor my associates/ employees shall not be liable for any losses incurred based on such opinions.

All matter displayed in this content is purely for Illustrative, Knowledge and Informational purpose and shall not be treated as advice or opinion of any kind.

The content presented should not be construed as investment advice unless explicitly stated in a client-specific research report. I or my employees/associates shall not be held liable/responsible in any manner whatsoever for any losses the readers may incur due to acting upon this content.

All information is taken from publicly available sources and data. I make no warranties or guarantees regarding the accuracy, completeness, or timeliness of the information provided, including data such as news, prices, and analysis. In no event shall I be liable to any person for any decision made or action taken in reliance upon the information provided by me.

We cannot guarantee the completeness or reliability of the information presented. Readers are encouraged to conduct their own research and consult with a professional advisor before making any investment decisions.